In the ever-evolving landscape of personal finance, loan refinancing has emerged as a powerful tool for homeowners seeking to optimize their financial health. Among the various forms of refinancing, a loan secured by real estate stands out as a particularly compelling option. This article delves into the intricacies of loan refinancing, specifically focusing on loans secured by real estate, and explores the associated risks and benefits. By the end of this read, you will have a comprehensive understanding of whether this financial maneuver is the right fit for your unique circumstances.

Understanding Loan Refinancing

Loan refinancing, at its core, is the process of replacing an existing loan with a new one, typically under different terms. The primary objective is to secure more favorable conditions, such as a lower interest rate, reduced monthly payments, or an altered loan term. When it comes to loans secured by real estate, the property itself serves as collateral, providing lenders with a sense of security and often resulting in more attractive terms for the borrower.

Imagine you are a captain navigating the vast ocean of financial obligations. Refinancing is akin to adjusting your sails to catch a more favorable wind, allowing you to reach your destination with greater ease and efficiency. However, just as a seasoned sailor must be aware of potential storms, a prudent borrower must be cognizant of the risks and benefits associated with refinancing a loan secured by real estate.

The Benefits of Loan Refinancing: Loan Secured by Real Estate

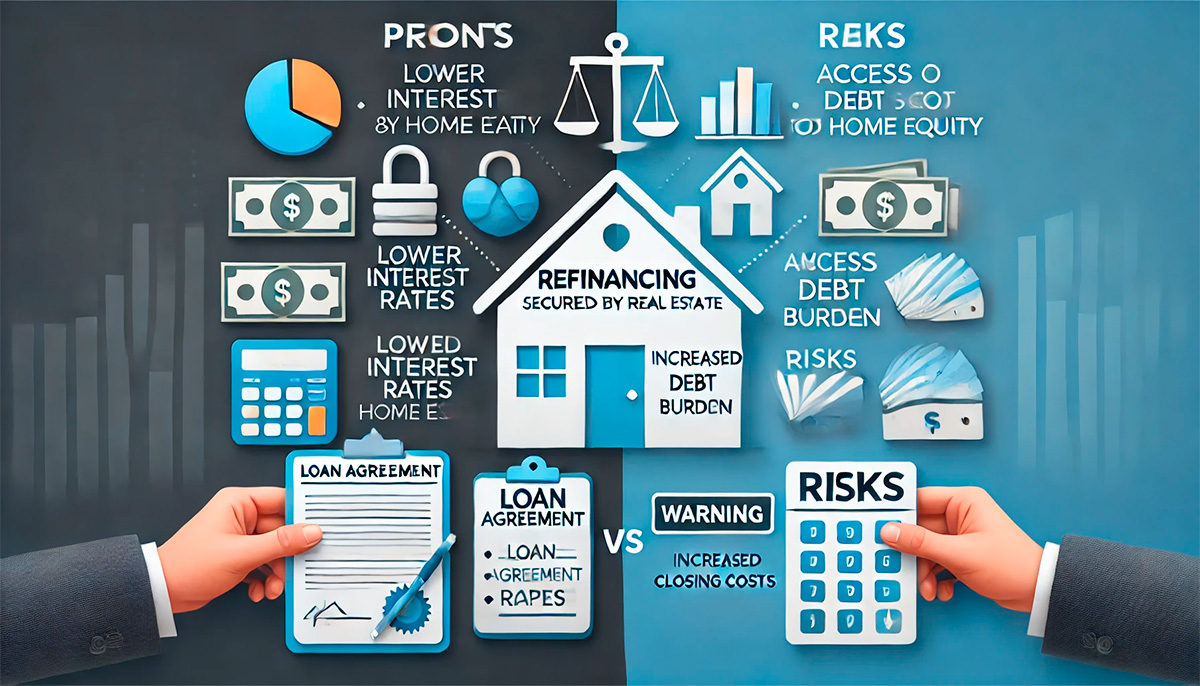

One of the most enticing benefits of refinancing a loan secured by real estate is the potential for significant interest savings. Interest rates are the lifeblood of any loan, and even a slight reduction can translate into substantial savings over the life of the loan. For instance, if you initially secured your mortgage during a period of high-interest rates, refinancing during a period of lower rates could save you thousands of dollars.

Another advantage is the possibility of lowering your monthly payments. This can be achieved either through a reduced interest rate or by extending the loan term. Lower monthly payments can free up cash flow, providing you with more financial flexibility to invest, save, or simply enjoy a higher quality of life. It’s like giving your budget a much-needed breather, allowing you to allocate resources to other pressing needs or aspirations.

Refinancing can also offer the opportunity to switch from an adjustable-rate mortgage (ARM) to a fixed-rate mortgage. ARMs can be unpredictable, with interest rates fluctuating over time. By refinancing to a fixed-rate mortgage, you lock in a consistent interest rate, providing stability and predictability in your financial planning. It’s akin to trading a rollercoaster ride for a smooth, steady journey.

Additionally, refinancing can enable you to tap into your home’s equity. If your property has appreciated in value, you may be able to secure a larger loan and access cash for major expenses such as home renovations, education, or even debt consolidation. This can be a strategic move to leverage your real estate investment for broader financial goals.

The Risks of Loan Refinancing: Loan Secured by Real Estate

While the benefits are compelling, it’s crucial to approach loan refinancing with a clear understanding of the potential risks. One of the primary concerns is the cost associated with refinancing. Closing costs, appraisal fees, and other expenses can add up, potentially offsetting the savings from a lower interest rate. It’s essential to conduct a thorough cost-benefit analysis to ensure that refinancing makes financial sense in your specific situation.

Another risk is the possibility of extending the loan term. While this can lower monthly payments, it also means you’ll be paying interest for a longer period, which could result in higher overall costs. It’s a bit like stretching out a rubber band—while it may provide immediate relief, the long-term tension could lead to greater strain.

Refinancing can also impact your credit score. The process typically involves a hard credit inquiry, which can temporarily lower your score. Additionally, if you’re not diligent about making timely payments on your new loan, your creditworthiness could suffer. It’s a delicate balancing act, requiring careful attention to maintain your financial health.

Moreover, there’s the risk of over-leveraging your property. Accessing your home’s equity can be a double-edged sword. While it provides immediate financial resources, it also increases your debt burden. If property values decline or your financial situation changes, you could find yourself in a precarious position, potentially facing foreclosure if you’re unable to meet your obligations.

Navigating the Decision: Is Refinancing Right for You?

Deciding whether to refinance a loan secured by real estate is a deeply personal choice, influenced by a myriad of factors. It’s essential to consider your long-term financial goals, current market conditions, and individual circumstances. Consulting with a financial advisor or mortgage specialist can provide valuable insights and help you make an informed decision.

Think of refinancing as a strategic chess move. It requires foresight, careful planning, and a clear understanding of the potential outcomes. By weighing the risks and benefits, you can determine whether this financial maneuver aligns with your broader objectives and sets you on a path toward greater financial stability and success.

Conclusion

Loan refinancing, particularly when secured by real estate, offers a wealth of opportunities to optimize your financial situation. From reducing interest rates and monthly payments to accessing home equity, the benefits can be substantial. However, it’s imperative to approach this decision with a clear-eyed understanding of the associated risks, including costs, extended loan terms, and potential impacts on your credit score and financial stability.

In the grand tapestry of personal finance, refinancing is but one thread, yet it can significantly influence the overall pattern. By carefully considering the risks and benefits, you can make a choice that enhances your financial well-being and brings you closer to your goals. Whether you’re seeking to save money, reduce monthly payments, or leverage your home’s equity, loan refinancing secured by real estate can be a powerful tool in your financial arsenal. Just remember, as with any financial decision, knowledge is your greatest ally.